3 ECS Key Application Areas

3.4

Health & Wellbeing

The healthcare industry is facing radical change, enabled by its current digital transformation in combination with a change towards a personalized medicine. Related developments will progressively generate a new ecosystem. New players will come to the fore, either from within the industry or through newcomers accessing the healthcare industry ecosystem.

Data will play an increasingly important role in providing a better understanding of consumer needs in terms of health, and to enhance and tailor a more cost-efficient health offering that delivers the right care at the right time and in the right place. The interconnections made possible by being able to access pools of data not previously available (worldwide database, data clouds, apps, etc.) are creating a major shift in healthcare provision.

A few years ago, the big techs (especially Google, Apple, Meta, Amazon and Microsoft) started to move into healthcare, which is a heavily regulated industry. The spread of digitalisation and innovative information technology (IT) is giving them the chance to enter the medical market. Data are everywhere, and healthcare practitioners need to cope with new and emerging digitalised delivery tools. Health tech companies, whether large corporations, small and medium-sized enterprises (SMEs) or start-ups, bring extensive expertise in using data and analytics, will be the dominant catalyst of these trends and are likely to drive change in the healthcare industry.

The Covid-19 pandemic is accelerating the adoption of telemedicine, initially at the most basic level (i.e. consultation by telephone), something that governments are also taking the opportunity to roll out, and this type of consultation is likely to further enable the digitisation of auscultations for medical diagnoses. Also, in a post Covid-19 era, regulators – usually seen as the main inhibitors – are also expected to be more favourable towards accelerating the current healthcare digital transformation.

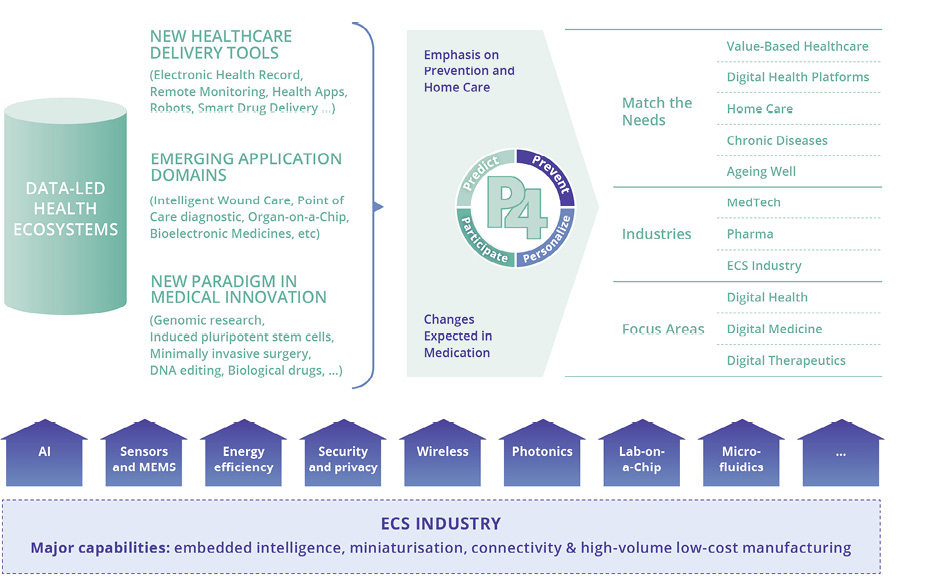

The emergence of so called P4 healthcare – predictive, preventive, personalised, participatory – as opposed to reactive healthcare, is blurring the lines between medical technology (medtech), the pharmaceutical industry and electronic components and systems (ECS) industry, opening the way for healthcare innovation. This is a huge opportunity for the European ECS industry, its worldwide medtech and pharma market leaders, as well as the 25,000 SME medtech companies across Europe, since the new healthcare ecosystem will rely189 on digital instruments, advanced electronic sensors and photonics, micro-electromechanical systems (MEMS), and the large volume, high-quality, low-cost production capabilities of the ECS industry.

3.4.2.1 External requirements

Healthcare electronics represents approximately 5% of global electronic equipment production, amounting to €91 billion in 2017 versus a total of €2,000 billion for the industry as a whole190. This report shows that healthcare is now the seventh biggest market in terms of electronic production worldwide, and is expected to benefit from a robust growth rate of over 5% over the next few years.

Within the industry, the current major innovation is the “big data” healthcare market. The market is exploding: the volume of generated data in healthcare is predicted to more than triple from 2017 (700 exabytes, i.e. 700 1018 bytes) to 2025 (2300 exabytes), according to a survey by BIS Research. This is supported by other studies, such as the “Stanford Medicine 2020 Health Trends Report”, which identifies the rise of the (digital) data-driven physician as a direct consequence of how data and technology is transforming the healthcare sector.

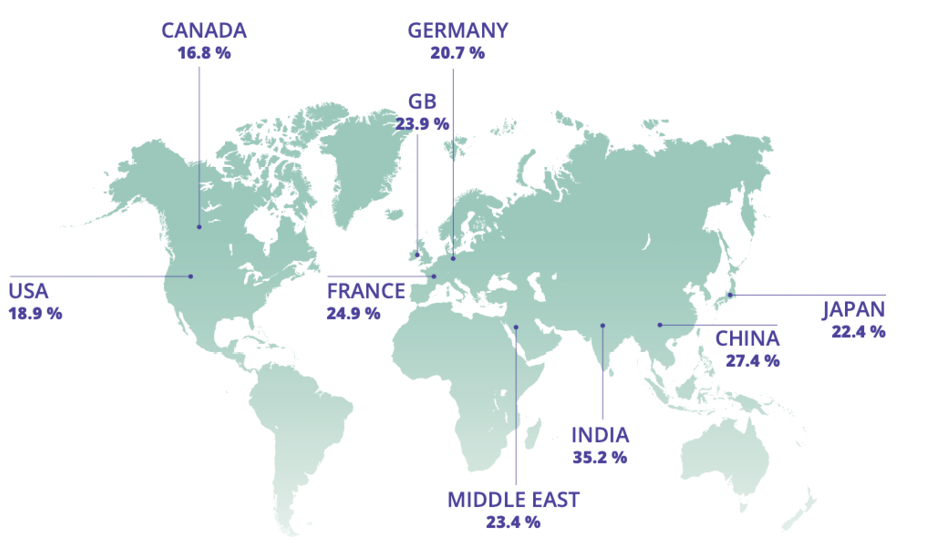

Of course, this big data trend in healthcare relies on government initiatives to encourage the adoption of digital health, and it is interesting to note that Europe – represented in the map of Figure F.74 by three countries behaving similarly – is well in line with the global trend.

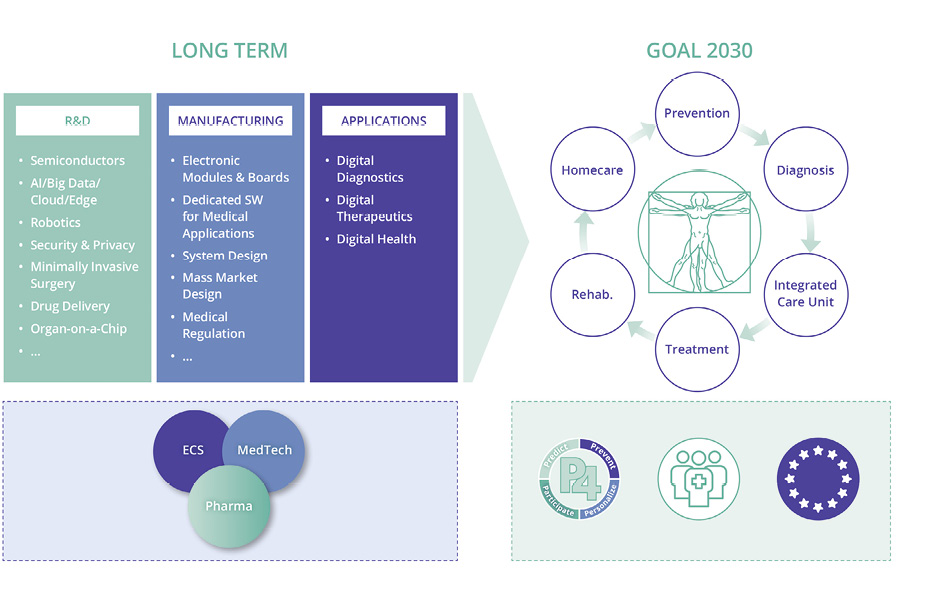

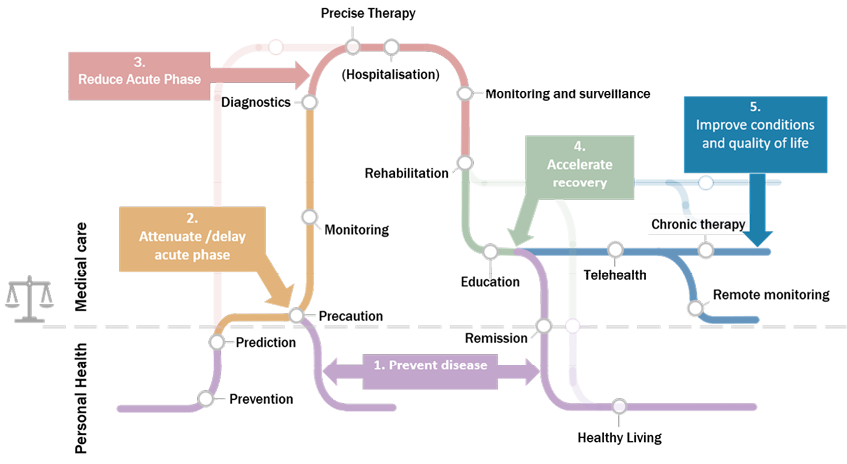

These trends in healthcare electronics, healthcare data and healthcare technologies will continue to impact the healthcare value chain. The graphic in Figure F.75 highlights how the healthcare digital transformation is gradually positioning the “healthcare consumer” at the centre of the value chain. It also shows how healthcare electronics – from research and development (R&D) to design and manufacturing – will digitalise the application segments, and how the care pathways – from prevention to treatment – will be transformed. As a consequence, healthcare will increasingly occur at the “point-of-need”, in most cases at home, whether for wellbeing, preventive measures or post-hospital intervention (e.g. rehabilitation) centred around the patient and taking place away from a clinical environment. Such a transformation will be enhanced by less of an obvious division between the ECS industry and the medtech and pharma ecosystems, as is also reflected in the Innovative Health Initiative Joint Undertaking, or IHI JU.

3.4.2.2 Societal benefits

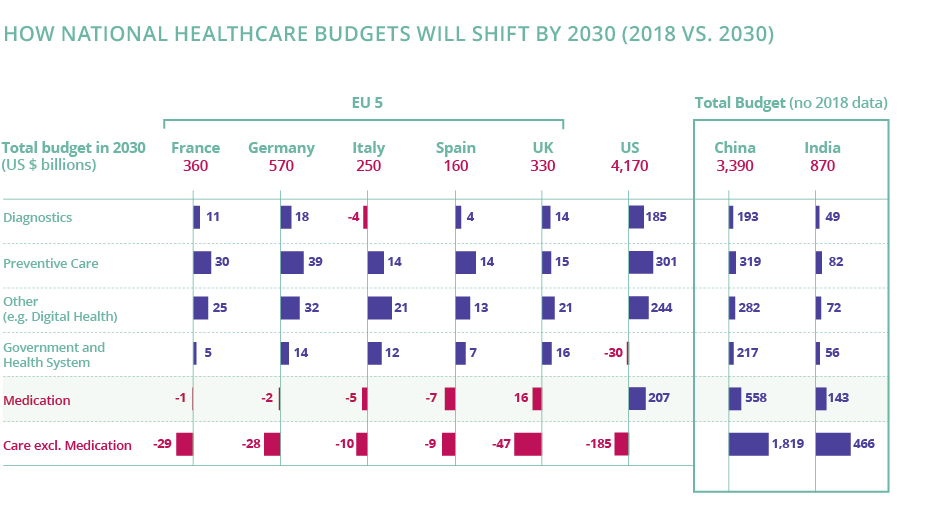

According to different projections, healthcare budgets around the world are expected to increase by 10% in aggregate by 2030. Healthcare spending will be driven by ageing and growing populations, rising labour costs, and by clinical and technology advances. Consequently, by 2030 healthcare is expected to be centred on patients being empowered to prevent disease rather than seek treatment, as highlighted above. Healthcare consumers will receive personalised health solutions provided within a healthcare system that is organised and regulated in an entirely new way (see Figure F.75).

Healthcare budgets in Europe will therefore shift towards novel areas such as digital health and more advanced prevention and rehabilitation options, for which home care will play a key role. Money is expected to be redirected toward personalised medicine for the most complex diseases, and preventive, early-stage treatments. This split is likely to lead to significant changes and require new R&D strategies for many industry players. The expectations will lie in those areas summarised in the Figure F.77.

Another societal benefit relates to medical education, an area rapidly progressing due to computer-assisted learning, student medical apps, digital games, simulation and wearable technologies increasingly being embedded in the curriculum, although the pace has not yet been fast enough to meet the clinical need. The Covid-19 crisis has exemplified the need for greater investment in technology to facilitate this. For example, recent events have highlighted the crucial role of anaesthesia in airway management to reduce fatalities, yet clinical airway management is constrained by insufficient training time. Simulation training in airway management is recommended by the Royal College of Anaesthetists, but in recent years less than half of NHS consultants in the UK have access to adequate training.

In addition to technical skills such as attention and manual dexterity, some non-technical skills (including situation awareness and cognitive communication) have been highlighted as contributory factors in airway management. Multidisciplinary team training has been advocated, but Covid-19 has highlighted the need for rigorous preparation for airway management through the inclusion of checklists and cross-checks, in addition to the need for highly skilled experienced airway operators to perform first-pass tracheal intubations. Although team-based training and simulation are critical to maximising successful outcomes, training that was previously considered to be occasionally necessary has gained in importance in critical care. Clinical engineering, simulator training and objective performance measures through non-invasive wearable sensors in training and practice is becoming progressively important for patient safety, with further key roles being in extended realities, robotics, Internet of Things (IoT) and Artificial Intelligence (AI). The clinical need and potential applications extend across clinical skills in areas such as needle intervention, surgery and radiology, as well as in non-technical skills in all areas of medicine.

Fostering the convergence of technologies will enable the development of cross-sectoral innovations more able to respond to people’s needs. Such an approach will also facilitate the integration of health interventions developed by different industrial sectors along the health care pathway. The goal is a more targeted intervention strategy leading to personalised treatments and improved individual health outcomes.

In total, research and innovation regarding ECS for health and well-being will play its part and is also indispensable for realization of specific objectives in healthcare as defined in the Strategic Research and Innovation agenda of the Innovative Health Initiative:

- Contribute towards a better understanding of the determinants of health and priority disease areas.

- Integrate fragmented health R&I efforts bringing together health industry sectors and other stakeholders, focussing on unmet public health needs, to enable the development of tools, data, platforms, technologies and processes for improved prediction, prevention, interception, diagnosis, treatment and management of diseases, meeting the needs of end-users.

- Demonstrate the feasibility of people-centred, integrated health care solutions.

- Exploit the full potential of digitalisation and data exchange in health care.

- Enable the development of new and improved methodologies and models for comprehensive assessment of the added value of innovative and integrated health care solutions.

In total, those objectives will contribute to the effort to both shorten the time a patient is actually in acute medical care and improve his or her conditions and quality of life (see Figure F.78).

Like the rest of the world, Europe is going through a healthcare digital transformation, creating a fundamental evolution in care delivery mechanisms. Digital innovation based on the EU’s ECS, medtech and pharma industries can support Europe’s response to some of the key technological challenges that will be discussed later in this Chapter, as well as the societal challenges lying ahead, as summarised above.

Europe is well-positioned in terms of electronic equipment dedicated to health and care (with 19% of global production in 2017). The European healthcare industry has a number of competitive advantages in a range of economic sectors related to health and social care, as well as digital technology. For example, some of the market leaders in medical equipment (Philips Healthcare, Siemens Healthineers) are Europe-based companies. The pharmaceutical industry is a major contributor to the European economy, with an estimated 1.4% of the EU’s combined GDP and 0.9% of the region’s employment (Source: EFPIA, 2019).

Programmes such as “EU4Health”, which is based in Brussels, are designed to ensure that the EU remains the healthiest region in the world, offering tools promoting innovation in the health sector – making medicines, medical devices and other crisis-relevant products available and affordable, supporting innovation and addressing other important long-term challenges for health systems. This particularly includes obstacles to a broader uptake and the best use of digital innovations, as well their scaling up, as Europe needs to become faster in the translation of ideas and valid technology into economically viable solutions.

Regulators are approving a growing number of digital health therapies, unleashing innovation in digital medicine and AI, which has the potential to transform the key steps of clinical trial design – from study preparation to execution, towards improving trial success rates – thus lowering the pharma R&D burden. For instance, in November 2019 Germany passed a law to allow doctors to prescribe health apps, with costs being reimbursed by insurers.

The European Commission has also adopted a Recommendation on a European Electronic Health Record (EHR) exchange format. This Recommendation seeks to facilitate the cross-border interoperability of EHRs in the EU by supporting members states in their efforts to ensure that citizens can securely access and exchange their health data wherever they are in the EU.

In order to unleash the full potential of health data, the European Commission has presented a regulation to set up the European Health Data Space (EHDS). EHDS is a health specific ecosystem comprised of rules, common standards and practices, infrastructures and a governance framework that aims at empowering individuals through increased digital access to and control of their electronic personal health data, nationally and cross-borders, as well as support to their free movement, fostering a genuine single market for electronic health record systems, relevant medical devices and high risk artificial intelligence (AI) systems (primary use of data) providing a consistent, trustworthy and efficient set-up for the use of health data for research, innovation, policy-making and regulatory activities (secondary use of data).

However, as we have recently seen, Europe still faces difficulties in reaction to pandemic situations, as for instance required protective goods are not available in number required to cope with the situation. This calls for a better integration of medical resources for pandemics, as the Covid-19 crisis has provided a big impetus for enabling digital health, prompting changes that are helping tech companies and data innovators play a greater role in service delivery. Nonetheless, the digital transformation of healthcare is only at its beginning.

Europe needs to maintain this momentum and build upon digital health technologies that will support this healthcare transition to reach market maturity and wide acceptance. They can help the EU to become faster in translating ideas into economically viable solutions, and which can be further scaled up in daily health practice. These are some of the main questions that have to be addressed to achieve this:

- How can the EU prepare its healthcare system to undertake digital transformation, managing a shift in focus from acute, hospital-based care to early prevention?

- How can the EU contribute to delivering cost-effective and high-quality healthcare, maximising the patient’s overall outcomes?

- How can the EU contribute to strengthening where and how healthcare is delivered, supporting home-based care?

- How can the EU support a much stronger participation of citizens in their own care process, enhancing patient engagement?

- How can the EU contribute to supporting its clinical workforce and healthcare consumers to embrace technology-enabled care?

This Chapter on the ECS health applications of the ECS-SRIA will provide recommendations to answer these questions from the perspective of technology, with the aim to establish Europe as a global leader:

- In P4 healthcare deployment, enabling digital health platforms.

- In the healthcare system paradigm transition from treatment to health prevention, enabling the shift to value-based healthcare.

- In building a more integrated care delivery system, supporting the development of the home as the central location of the patient.

- In enhancing the access to personalised and participative treatments for chronic and lifestyle- related diseases.

- In ensuring a healthier life for an ageing population.

Five Major Challenges have been identified for the healthcare and wellbeing domain:

- Major Challenge 1: Enable digital health platforms based upon P4 healthcare.

- Major Challenge 2: Enable the shift to value-based healthcare, enhancing access to 4P’s game-changing technologies.

- Major Challenge 3: Support the development of the home as the central location of the patient, building a more integrated care delivery system.

- Major Challenge 4: Enhance access to personalised and participative treatments for chronic and lifestyle-related diseases.

- Major Challenge 5: Ensure more healthy life years for an ageing population.

3.4.4.1 Major Challenge 1: Enable digital health platforms based upon P4 healthcare

The medtech industry is in the process of transitioning from an industry primarily producing high-end hospital equipment to one that will increasingly serve point-of-care (PoC) professionals and “health consumers”, thereby moving from a product-based approach to the provision of “integrated services”.

Electronic medical technology, such as the Internet of Medical Things (IoMT), minimally invasive implants, energy-efficient devices, advanced analytics, cognitive computing for advanced clinical decision support, cybersecurity, enhanced network capabilities for continuous data access (to mention only a few of those listed below in the section “Key focus areas”), will support the deployment of P4 healthcare in a data-led environment.

The P4 healthcare vision is therefore not only placing doctors and other health professionals at the centre of the care process, but all those relevant to the health consumer. Even if the healthcare ecosystem is operating in a highly regulated environment, by 2030 we can expect this trend to progressively become the norm. The ECS community should participate in the development of dynamic healthcare systems that learn in real time from every result, achieve a better understanding of treatment response and prognostic heterogeneity, and introduce more refined, patient-tailored approaches to disease detection, prevention, and treatment.

The P4 healthcare vision, enabling for instance early diagnostics based upon merged data and machine-learning techniques through the detection of weak signals, allows preventive treatments that are far less intensive than acute treatments and increase the chances of survival and quality of life. The medtech industry is not alone on this journey. New pharmaceuticals and treatments will be developed for personalised medicine settings by embedding connected devices and exploiting the potential of the IoT and AI.

This is all creating a new industry, one that revolves around digital health platforms. This platform-based new market disruption will enable the emergence of specialised platforms, and new players will enter the health domain. This will impact current business models in healthcare, using aggregated data to create value rather than devices – supporting, for instance, proactive services, facilitating outcome evaluation for the treatment of different therapies, and paving the way for outcome-based or pay-per-use reimbursements. This is a potential path to reducing the burden of healthcare expenditures.

The addition of AI capabilities – person-centred AI-based consumer devices/embedded AI-based medical devices and systems – to Smart Things will significantly enhance their functionality and usefulness, especially when the full power of such networked devices is harnessed – a trend that is often called “edge AI”. AI enables much more efficient end-to-end solutions by switching from a centralised to a distributed intelligence system, where some of the analysis carried out in the cloud is moved closer to the sensing and actions. ![]()

This distributed approach significantly reduces both the required bandwidth for data transfer and the processing capabilities of cloud servers. It also offers data privacy advantages, as personal source data is pre-analysed and provided to service providers with a higher level of interpretation. It also offers greater reliability and safety.

A high level of digital trust – for privacy and security by design, hardened and embedded AI models – is of course required for executing transactions in healthcare and wellbeing. Securing the IoT ecosystem is a multiple level problem. Privacy should be “by design”. In general, integrating security features into an existing system can become very complex, sometimes impossible, and often increases the cost of the final product significantly. A more efficient approach is to consider those security requirements at the very beginning of a project, and then integrate them in the design and development phase. The ECS industry can assist with end-to-end solutions by providing on-chip security, supplying comprehensive hardware and software services, including authentication, data encryption and access management. ![]()

![]()

Next-generation connectivity – better performing, more ubiquitous, accessible, secure, and energy-efficient networks – will contribute to unleashing the potential of digital health. One of the main characteristics of future networks will be their increased intelligence to improve the performance of the networks, and offer sophisticated and advanced services to the users, due to edge computing and metadata, for instance. ![]()

With the significantly growing number of wearables and other small form-factor, battery-operated devices, very low power consumption is a major technology challenge for product designers. The transition from linear to circular economy will require innovative designs for the lifetime of electronic components and systems, and disruptive changes in ECS supply chains, to reduce the ecological footprint. The ECS industry will contribute to improving energy efficiency – including new, sustainable, and biocompatible energy harvesting – to locally process data and the transmission of pre-processed data as opposed to the transmission of high-volume data (such as imaging data). ![]()

![]()

As a result of improved integration and analysis of multimodal data, new tools for clinical decision-making and precision medicine will emerge, supporting early diagnostics, personalised medicine and potential curative technologies (e.g. regenerative medicine, immunotherapy for cancer).

3.4.4.2 Major Challenge 2: Enable the shift to value-based healthcare, enhancing access to 4P’s game-changing technologies

A major trend in healthcare is the transformation of large healthcare systems to an optimised hospital workflow: a shift from general hospitals treating any diseases towards integrated practice units that specialise in specified disease types. These units, organised around a medical condition, aim to maximise the patient’s overall outcomes as efficiently as possible, increasingly through remote access, for patients anywhere in the world.

Pay-for-cure rather than pay-for-treatment can be an effective way to increase the efficiency of healthcare by avoiding unnecessary tests, therapies, and prescriptions. Combined with empowered patients, care-givers should be able to make better informed and more effective choices for treatment. To achieve this, outcomes need to cover the full cycle of care for the condition and track the patient’s health status aftercare is completed. This first involves the health status, relying for instance on EHRs supporting precise communication between different care-givers’ PoC diagnostic systems or AI-based clinical decisions. Early diagnosis is key for the successful treatment of both modest and challenging medical conditions.

Health outcomes are also related to the recovery and the sustainability of health. Readmission rates, level of discomfort during care, and return to normal activities should be taken into account for both providers and patients. Humanoid robots applying interpreted human body language and emotion in care delivery, sensors, the deployment of companion devices anticipating and contextualising acute or chronic conditions in EHRs involving health models describing the outcome health values for the patients, both in the short term and long term, will have a direct positive effect on readmission prevention.

To achieve this transformation, a supporting IT platform is necessary. Historically, healthcare IT systems have been siloed by department, location, type of service, and type of data (for instance, diagnostic imaging). An innovative and efficient healthcare information infrastructure – integrating IoT with big data learning for optimising workflow, usage, capabilities and maintenance, and of course digital trust – will aggregate the different areas for efficient value-based healthcare, combining prevention tools, early detection, and treatment. This will enable better measurement and facilitate the design and implementation of new bundle-based reimbursement schemes, reducing costs while improving health outcomes. By 2030, value-based healthcare will enable the adoption of optimisation practices already supported by ECS technologies in the industry. ![]()

By 2030, clinical decision-making will be augmented by electronic medical records. Digital centres will enable advanced capabilities for clinical decision-making where AI, real-time data from portable Point-of-Care devices, 3D printing for surgeries, continuous clinical monitoring – including robotics to improve treatments either in the operating room, minimal invasively inside the body, at the general practitioner or at home – will support the integration of specialised care units. A large number of images will be combined with other sensor data and biomedical models to obtain precise, quantified information about the person’s health condition, preventing and providing, for instance, early warnings for (combined) diseases supported by patient health models on complex health conditions. Low–latency, massive image processing is a major information source for AI-based automation, visualisation, and decision support within the whole care cycle. Precise quantified and annotated imaging is needed at many levels: from molecular imaging up to whole body imaging. The development and use of accurate digital twins of the human body will enable clinical trials, individualised computer simulations used in the development or regulatory evaluation of a medicinal product, device, or intervention. While completely simulated clinical trials are not yet feasible, their development is expected to have major benefits over current in vivo clinical trials, which will drive further research on the subject. Moreover, ”digital twins” will help in combining all the data on a personal level, and enable personalised clinical decision-making.

Europe is a leading producer of diagnostic imaging equipment. In diagnostic imaging, the ECS industry has begun to place great emphasis on accurate radiation dose monitoring and tracking. Healthcare providers are already applying dose management as part of the quality programme in their radiology departments, and patient-specific computed tomography (CT) imaging and personalisation of scan protocols will be a key aspect of patient- centred care in radiology departments, facilitating the management and control of both image quality and dose with the optimisation of 3D X-ray imaging protocols. In particular, CT and X-ray systems based on the emerging spectral X-ray photon counting technology will enable new ways of imaging in order to reduce dose, improve tissue differentiation, enhance visualization, or quantify materials.

The enormous capabilities of the ECS industry in miniaturisation, integration, embedded intelligence, communication and sensing will have a major impact on the next generation of smart minimally invasive devices: ![]()

![]()

- Highly miniaturised electrical and optical systems realised using advanced cost-effective platform technologies will bring extensive imaging and sensing capabilities to these devices, and enable the second minimally invasive surgery revolution, with smart minimally invasive catheters and laparoscopic instruments for faster and more effective interventions.

- Sensing and diagnostics solutions need to achieve appropriate sensitivity, specificity, and time-to-result.

- Reducing waste is possible through sensors made of biological materials, combining a biological component with a physicochemical detector.

- Fusion of diagnostics and surveillance will help reducing system and operational costs.

- To realise next-generation smart catheters, a broad spectrum of advanced ECS capabilities will need to be brought together, foremost in dedicated platforms for heterogeneous miniaturisation and integrated photonics. These can be complemented with platforms for embedded ultrasound, low-power edge computing, and AI and digital health platform integration.

- Optical coherence tomography (OCT) is another example where ECS technologies make a critical impact, in shrinking devices and reducing costs, allowing devices to be used in wider fields beyond ophthalmology.

Finally, it should be noted that the development of the next generation of smart minimally invasive instruments will go hand in hand with the development of new navigation techniques: ![]()

![]()

![]()

- Breakthrough innovations in photonics are enabling optical shape-sensing techniques that can reconstruct the shape of a catheter over its entire length.

- MEMS ultrasound technology will enable segmented large-area body conformal ultrasound transducers that are capable of imaging large parts of the body without the need for a trained sonographer, to guide surgeons in a multitude of minimally invasive interventions.

- Combined with other technologies, such as flexible and conformal electronics, low power edge computing, AI, and data integration into clinical systems, new optical and acoustic- based technologies may eliminate the use of x-rays during both diagnosis and interventions, enabling in-body guidance without radiation.

- Augmented reality can be used for image-guided minimally invasive therapies providing intuitive visualisation.

As mentioned above, outcomes should cover the full cycle of care for the condition and track the patient’s health status once care has been completed. Biomarkers derived from medical images will inform on disease detection, characterisation, and treatment response. Quantitative imaging biomarkers will have the potential to provide objective decision-support tools in the management pathway of patients. The ECS industry has the potential to improve the understanding of measurement variability, while systems for data acquisition and analysis need to be harmonised before quantitative imaging measurements can be used to drive clinical decisions.

Early diagnosis through PoC diagnostic systems represents a continuously expanding emerging domain based on two simple concepts: perform frequent but accurate medical tests; and perform them closer to the patient’s home. Both approaches lead to improved diagnostic efficiency and a considerable reduction in diagnostic costs:

- Point-of-care testing (PoCT) methodology encompasses different approaches, from the self-monitoring of glucose or pregnancy, to testing infectious diseases or cardiac problems. However, it should be remembered that disposable PoC devices will need to be environmentally friendly in terms of plastic degradation and the replacement of potentially harmful chemicals.

- The key enabling components of current PoCT devices must include smart and friendly interfaces, biosensors, controllers, and communication systems, as well as data processing and storage.

- The emerging lab-on-a-chip (LoC) solutions, embedding multiple sensor platforms, microfluidics, and simple processing/storage elements, are currently the most promising basis for the realisation and development of accurate, versatile, and friendly portable and wearable PoCT devices. Their simplified operation mode eliminates the constraint of molecular biology expertise to perform a real-time reverse transcription polymerase chain reaction (RT-PCR) test, will enable innovative in vitro diagnostic (IVD) platforms, making possible decentralisation from highly specialised clinical laboratories to any hospital lab and near- patient sites, with dedicated sample prep cartridges, a more efficient prevention (referring to the recent Covid-19 pandemic) and prompt personalised diagnosis.

In addition, digital supply chains, automation, robotics, and next-generation interoperability can drive operations management and back-office efficiencies. Using robotics to automate hospital ancillary and back-office services can generate considerable cost and time efficiencies, and improve reliability. Robotic process automation (RPA) and AI can allow care-givers to spend more time providing care. For instance, robots can deliver medications, transport blood samples, collect diagnostic results, and schedule linen and food deliveries – either as a prescheduled task or a real-time request. Robotic processes also can be used for certain hospital revenue cycle and accounting/finance functions, such as scheduling and claims processing.

3.4.4.3 Major Challenge 3: Support the development of the home as the central location of the patient, building a more integrated care delivery system

The trend towards integrated practice units specialising in specific disease types as described in the previous challenge means that certain procedures can move out of the hospital environment and into primary care and home care. Medical equipment that was previously used only in the hospital or clinic is finding its way into the home. For example, tremendous progress has been made since the “consumerisation” of the MEMS in developing compact, accurate, low-cost silicon sensors and actuators. This continuous innovation will support diagnostic and treatment in integrated practice units, while supporting recovery and health sustainability at home. This trend will be supported by the integration of solutions and services for specific disease groups with hospital units to optimise patient-generated health data (PGHD: continuous monitoring, clinical trials at home, etc), enhanced by the integration of heterogeneous devices and systems used at home covering parts of the care cycle (smart body patches, monitoring implants, remote sensing, etc). Solutions are needed that can be integrated into secure health digital platforms, portable end-user devices, remote e-healthcare and AI front-ends.

In addition, the pharmaceutical market is experiencing strong growth in the field of biologics (genomics and proteomics, as well as microarray, cell culture, and monoclonal antibody technologies) that require preparation prior to administration. Smart drug delivery solutions are now based on innovative medical devices for the automated and safe preparation and administration of new fluidic therapies and biologic drugs. These use advanced ultra-low power microcontrollers that control the process reconstitution of the drug based on parameters identified by the practitioner, together with wireless communication modules to transmit data and ensure the patient and treatment are monitored. Smart drug delivery will improve drug adherence as patients will be empowered to administer expensive and complex drugs in their own home.

In this emerging context, care solutions need to be integrated, combining information across all phases of the continuum of care from many sources – preventing, preparing, and providing care based on person-specific characteristics. This will support the development of applicable biomedical models for specific disease groups, for customer groups and for populations, taking heterogeneous data involving history, context, or population information into account. ![]()

Supporting prevention, diagnosis and aftercare with sensors and actuators to ensure efficient medical decision, leveraging edge computing and imaging as described in the previous section, will be crucial. The next generation of devices will incorporate increasingly powerful edge computing capabilities. Analysing PGHD from medical devices can be synchronised with a web-based monitoring system. When aggregated, this data can be then sent to the organisation’s health data analytics system to process the results and compare them to previous measurements. If the analysis uncovers negative trends in the patient’s health status, it will automatically notify the care team about possible health risks. The ECS industry can play an important role here in bringing ambulatory monitoring to the next level. The following enabling technology platforms can contribute to this: ![]()

![]()

![]()

![]()

- Low-power technology for sensors, microprocessors, data storage and wireless (microwave, optical, sound) communication modules, etc.

- Miniaturisation and integration technologies for sensors, microprocessors, data storage, and wireless communication modules, etc.

- Advanced sensing technologies for multiplex, painless sensing with high sensitivity and reliability.

- Printed electronics technology for textile integration and the patch-type housing of electronics.

- Low-power edge AI computing for data analysis and reduction.

- Data communication technology for interoperability of (wireless) data infrastructure hardware (wearable device connections) and software (data sharing between data warehouses for analysis, and with patient follow-up systems for feedback).

- Data security technology for interoperability between security hardware and software components (end-to-end information security).

The development of next-generation drug delivery systems will form part of the IoMT – medical devices and applications that link with healthcare systems using wireless connectivity. Smart drug delivery will improve drug adherence so that patients can administer expensive and complex (biological) drugs in their home environment. Enabling platforms are required to facilitate a transition from the legacy mechanical components seen in current autoinjectors and wearable drug delivery pumps, to highly integrated, patch-like microsystems. These include: ![]()

![]()

- High-performance sensors and actuators for drug delivery, monitoring and control.

- On-board microfluidics for in situ preparation and delivery of formulations.

- Minimally invasive needles and electrodes for transdermal interfacing, delivery, and diagnostics.

- New materials, containers and power sources that will meet stringent environmental and clinical waste disposal standards.

- Body-worn communication technologies for IoMT integration and clinical interfacing.

- Edge AI for closed-loop control, adherence assessment and clinical trial monitoring.

The development of low-cost, silicon-based MEMS ultrasound transducer technologies is bringing ultrasound diagnostics within the reach of the ECS industry. The ECS industry has the instruments and production technologies to transform these into high-volume consumer products, something no other industry is capable of. Personal ultrasound assisted by AI data acquisition and interpretation will allow early diagnoses in consumer and semi-professional settings, as well as in rural areas. As such, they present a huge opportunity for the ECS industry. It is expected that MEMS ultrasound will enable a completely new industry, with MEMS ultrasound transducers being the enabling platform technology that will drive things on.

Among the emerging applications of advanced medtech, “smart wound care” – i.e. the merger of highly miniaturised electronic, optical and communications technologies with conventional wound dressing materials – will allow the treatment of chronic wounds of patients in their home without the intervention of daily nursing and/or constant monitoring of the status of the wound. While much progress has been made in wearable technologies over the past decade, new platforms must be developed and integrated to enable the rapid rollout of intelligent wound care. These include: ![]()

![]()

![]()

- Flexible and low-profile electronics, including circuits, optical components, sensors, and transducers, suitable for embedding within conventional dressings.

- Advanced manufacturing techniques for reliable integration of microelectronic technologies with foam- and polymer-based dressing materials.

- Biodegradable materials, substrates, and power sources that will meet stringent environmental and clinical waste disposal standards.

- Body-worn communications technologies for low-power transmission of wound status.

- Edge AI to assist the clinical user in data acquisition and data interpretation.

3.4.4.4 Major Challenge 4: Enhance access to personalised and participative treatments for chronic and lifestyle-related diseases

According to the World Health Organization (WHO) definition, chronic diseases are those of long duration and generally slow progression. Chronic diseases such as heart disease, stroke, cancer, chronic respiratory diseases, and diabetes are by far the leading cause of mortality in Europe, representing 77% of the total disease burden and 86% of all deaths. These diseases are linked by common risk factors, common underlying determinants, and common opportunities for intervention.

One of the crucial means of coping with the prevalence of the chronic diseases is to achieve a more participative and personalised approach, as such diseases require the long-term monitoring of the patient’s state, and therefore need individuals to take greater ownership of their state of health. Most chronic disease patients have special healthcare requirements and must visit their physicians or doctors more often than those with less serious conditions. Technological innovation has already been identified as a great medium to engage chronic patients in the active management of their own condition since digital health offers great convenience to such patients. Access to biomedical, environmental and lifestyle data (through cloud computing, big data and IoT, edge AI, etc) are expected to better target the delivery of healthcare and treatments to individuals, and to tailor each decision and intervention, especially for the treatment of those with multiple chronic diseases.

Patients will be connected seamlessly to their healthcare teams, care-givers and family, as treatment adherence will be more efficient with the innovations mentioned in previous sections. Remote sensing and monitoring offer great promise for the prevention and very early detection of pathological symptoms. Remote sensing and monitoring have the potential to become embedded into everyday life objects, such as furniture and TV sets, while bearing in mind the constraints related to security and privacy. Remote patient monitoring will support clinical decisions with a reduced potential for false alarms, especially for the long-term monitoring and data analysis of patients with chronic diseases. ![]()

![]()

The ECS industry will need to take the initiative in the development of the next-generation treatment of chronic diseases. The field of remote sensing holds great promise for the lifelong and chronic monitoring of vital signs. The deployment of remote monitoring system relies on sensors integrated into bed or chair. Optical sensing techniques, for instance for remote reflective photoplethysmography, as well as capacitive and radar sensing support this approach. This will be multimodal, with fusing techniques to smart analytics to unify the data into usable information. The strength of remote sensing not only relies on the quality of the acquired signals, but also its potential to reveal slowly changing patterns – possibly symptoms from underlying physiological changes. The analysis of such datasets, currently largely unexplored, will provide new insights into normal versus pathological patterns of change over very long periods of time: ![]()

![]()

- Treatment of chronic diseases will be enhanced by an upcoming generation of small and smart implantable neuromodulator devices, which are highly miniaturised, autonomous, and cost-effective. These will be implanted, wirelessly powered by radio frequency (RF), microwave, ultrasound or energy harvesting with minimal side effects on the selected nerve through a simple and minimally invasive procedure to modulate the functions of organs in the treatment of pain management, brain disorders, epilepsy, heart arrhythmia, autoimmune diseases (immunomodulation), etc.

- Organ-on-a-chip (OOC) platforms, which lie at the junction of biology and microfabrication and biology for personalised and safer medicines, are another treatment approach, addressing, for instance, pathologies currently without effective treatment (rare diseases). Often rare diseases are chronic and life-threatening, and they affect approximately 30 million people across Europe. In an OOC, the smallest functional unit of an organ is replicated. The essential capabilities underlying the OOC field are primarily embedded microfluidics and the processing of polymers in a microfabrication environment. Smart sensors can be used as readout devices, while edge AI will be essential in data interpretation and reduction.

For chronic diseases diagnoses, LoC-based technologies – relying on miniaturisation – show promise for improving test speed, throughput, and cost-efficiency for some prominent chronic diseases: chronic respiratory diseases, diabetes, chronic kidney diseases, etc.

3.4.4.5 Major Challenge 5: Ensure more healthy life years for an ageing population

In the last two decades, effort has been made to enhance two important and specific objectives of smart living environment for ageing well:

- Avoid or postpone hospitalisation by optimising patient follow-up at home.

- Enable a better and faster return to their homes when hospitalisation does occur.

The following list includes some typical examples of assistance capabilities related to major chronic diseases covering the first main objective (optimisation of patient follow-up at home):

- Vital signs checker: blood pressure meter, oximeter, thermometer, weight scale.

- Hospital's software interface, the patient’s file, the patient's risk alarm centre with automatic call to healthcare practitioners.

- Video communication support (between the patient and their nurse, doctor, and family), and interactive modules for the patient (administrative, activities, menus, medical bot chat, etc.).

- Authentication and geolocation of patients, with patient or patient’s family consent.

- Teleconsultation for nights and weekends at the foot of the bed of patient’s hospital or retirement home.

The second objective – smooth home return – relates to suitable technical assistance in addition to human assistance:

- Enhance the patient's quality of life and autonomy.

- Improve the patient's safety and follow-up in their room through a reinforced work organisation.

- Allow monitoring of the patient’s progress to motivate them during their rehabilitation period.

- Minimally invasive therapies allowing for shorter hospital stays and improved patient wellbeing.

- First-time-right precision diagnoses to prevent hospital readmissions.

- Prepare for the return home: patient support in appropriating technical aids by integrating these solutions into rehabilitation.

Efforts are being made to enhance medical and social care services through different kinds of robots. The purpose here is to provide advanced assisted living services via a general-purpose robot as an autonomous interaction device that can access all available knowledge and cooperate with digital appliances in the home. In this sense, autonomous mobile robots offer several advantages compared to the current (stationary) Ambient Assisted Living (AAL) solutions. Due to sensor-augmented user interfaces, human computer interaction is becoming increasingly natural. As a consequence, robots will come to represent a familiar metaphor for most people.

Neurorehabilitation is sometimes required after hospitalization and is generally a very complex and challenging undertaking resulting in both “successes” and “failures” (setbacks). Neurological patients typically report having “good days and bad days”, which affect performance, motivation and stamina, and where cognitive stimulation (AI-based speech producing programs, social robots, etc), for example, has the potential to improve the efficiency of neurorehabilitation and relieve some of the pressure on health systems. Robotics is well suited for precise, repetitive labour, and its application in neurorehabilitation has been very successful. This is one of the main reasons why the rehabilitation robotics market has tripled over the last five years and, today, rehabilitation robotics is one of the fastest growing segments of the robotics industry. This industry is dominated by European companies that can deliver highly innovative solutions with a strong scientific basis and exceptional manufacturing quality. Based on market size and need, it is projected that the compound annual growth rate (CAGR) for rehabilitation robotics will soon reach between 20% and 50%.

The ECS industry can significantly upscale the “ageing well” area, as it is enabled by most of the focus topics developed in the previous sections. The industry is playing an important role in bringing ambulatory monitoring to the next level. Important aspects here are reducing costs, improving user friendliness (e.g. easy to wear/use devices, interoperable gateways, reduction of patient follow-up systems) and data security.

The enabling technology platforms detailed below are expected to significantly contribute to this prevalence of the ECS industry in ageing well, taking into account that ageing well is very much related to “ageing in place”: ![]()

![]()

![]()

![]()

- Low-power technology for sensors, microprocessors, data storage and wireless communication modules, etc.

- Miniaturisation technology for sensors, microprocessors, data storage and wireless communication modules, etc.

- Printed electronics technology for textile integration and patch-type housing of electronics.

- Low-power edge AI computing for data analysis and data reduction.

- Data communication technology for interoperability of (wireless) data infrastructure hardware (wearable device connections) and software (data sharing between data warehouses for analysis and with patient follow-up systems for feedback).

- Data security technology for interoperability between security hardware and software components.

- Robotics systems enabling patients to overcome loneliness or mental healthcare issues.

Interoperability is surely the main challenge faced by the ECS industry in achieving full impact due to the vast heterogeneity of IoT systems and elements at all levels. Interoperability and standardisation need to be elaborated in relation to data and aggregated information. Thus, it is not enough to be able to receive a message, i.e. to understand the syntax of the message, but it is also necessary to understand the semantics. This requirement implies the development of a data model that maps semantic content from the data received from devices into an information system that is usually utilised for collecting and evaluating data from monitored persons. It must be based on several relatively simple principles: creation of formats and protocols for exchange of data records between healthcare information systems; format standardisation and connected interface unification; improvement of communication efficiency; a guide for dialogue between involved parties at interface specification; minimisation of different interfaces; and minimisation of expenses for interface implementation. ![]()

The following table illustrates the roadmaps for Health and Wellbeing.

|

MAJOR CHALLENGE |

TOPIC |

SHORT TERM (2023–2027) |

MEDIUM TERM (2028–2032) |

LONG TERM (2033 AND BEYOND) |

|

Major Challenge 1: |

Topic 1: Establish Europe as a global leader in personalised medicine deployment |

|

|

|

|

Major Challenge 2: from treatment to health promotion and prevention |

Topic 2: Enable the shift to value-based healthcare |

|

|

|

|

Major Challenge 3: Home becomes the central location of the “healthcare consumer” |

Topic 3: Build an integrated care delivery system |

|

|

|

|

Major Challenge 4: ECS industry supports EU strategy to tackle chronic diseases |

Topic 4: Enhance access to personalised and participative treatments for chronic and lifestyle-related diseases |

|

|

|

|

Major Challenge 5: ECS industry fosters innovation and digital transformation in active and healthy ageing |

Topic 5: Ensure more healthy life years for an ageing population |

|

|

|

Close collaboration will be useful in all application areas – for example, Mobility, Energy, Digital Industry, Agrifood and Natural Resources, and Digital Society – based on cross-sectional technologies such as Edge Computing and Embedded Artificial Intelligence, Connectivity and, of course, Quality, Reliability, Safety and Cybersecurity. ![]()

![]()

![]()

![]()

More specifically:

- Related to digital industry, “bio-production”, which has the objective of developing an innovative field to produce the biologic products of the future through the implementation of disruptive technologies, should be an important topic to address in future years.

- The relationship between food systems and health is obvious and well-identified, especially in preventative health. This is an aspect that needs to be followed to reinforce health prevention in the long term.

- In terms of energy and connectivity, it is important to consider the impact of innovative wearables and implantables, sensors and actuators in general, as they represent a crucial sector with a direct impact on the further development of digital health.

- Embedded systems are an essential enabler of healthcare digital transformation. Medical systems have special requirements regarding hardware quality and reliability, dependability in connected software and human/ systems interaction. Also, privacy and cybersecurity are required to support the expansion of digital health. Related challenges are defined in the transversal Chapter Quality, Reliability, Safety and Cybersecurity.

189 Emerging Medical Domains for the ECS industry – Health.e lighthouse: www.health-lighthouse.eu Medtech Europe: www.medtecheurope.org

190 Study on the Electronics Ecosystem – Overview, Developments and Europe’s position in the world – Annex 4, Health & Care – Decision Etudes Conseil / CARSA

191 Electronic medical record (EMR): A computerised database that typically includes demographic, past medical and surgical, preventive, laboratory and radiographic, and drug information about a patient. It is the repository for active notations about a patient's health. Most EMRs also contain billing and insurance information, and other accounting tools.