2 CROSS-SECTIONAL TECHNOLOGIES

2.2

Connectivity

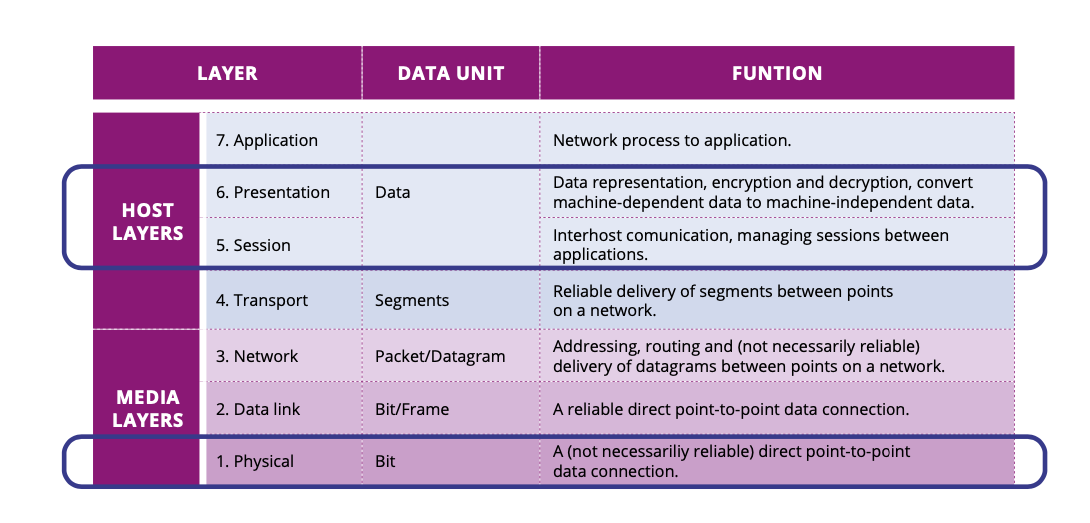

Connectivity and interoperability technologies in ECS enabling business and social benefits are tied to layers 1, 5, and 6 of the OSI model. The focus on these layers is motivated by the Major Challenges that characterise them (see Figure 1).

2.2.1.1 Scope for OSI layer 1

The scope covers the following types of physical layer connectivity.

-

Cellular:

-

Beyond 5G.

-

Early 6G investigation.

-

-

Low power wide area:

-

Cellular: narrow band IoT, LTE, 6G, etc.

-

Non-cellular: SigFox, LoRa, M-Bus, etc.

-

-

Low power short range:

-

Wireless: existing (Bluetooth, WiFi, etc.) or innovative technologies (mmW, etc.).

-

Wired: covering both high-speed optical glass and plastic fibers, mmW plastic fibers, and copper interconnect (USB, DOCIS, etc.).

-

-

High speed:

-

Wireless: point to point mmW and satellite communication (low earth orbit and geosynchronous equatorial orbits).

-

Wired: high-speed optical (400 Gb+, etc.) and copper interconnect (Ethernet, etc.).

-

The main challenge will be to ensure European leadership in terms of connectivity technologies (for example, standards) as well as associated software and hardware technology supporting the development of connectivity solutions (e.g. chipset, module, protocols, etc.).

2.2.1.2 Scope for OSI layer 5 and 6

The scope addressed in this context is the interoperability from application to application relying on technologies at OSI layers 5 and 6. This interoperability covers the following underlying aspects:

-

Protocols at all technology levels: Internet, operational and legacy.

-

Security: such as protocol security, payload encryption, certificates, tokens and key distribution.

-

Data semantics: supporting application to application understanding of transferred data/information.

Beyond their economic impact, connectivity and interoperability are also expected to play a key role in many societal challenges to be faced in the coming decades. As will be illustrated in this Section, the societal benefits associated with connectivity are key assets for improving the living standard of European citizens, as well as maintaining Europe leadership in this area.

-

Industrial competitiveness: the industrial transition to Industry 4.0/5.0, with its massive usage of automation and digitalization accompanied by AI-supported analytics, puts much higher demands on the availability and reliability of high-speed, secure, low or guaranteed latency connectivity. Given the large amount of legacy connectivity and emerging new connectivity, interoperability over technology generations and between application domains will become an enabler for competitiveness.

-

Healthcare improvement: connectivity has the potential to improve medical behaviour for patients and healthcare professionals, as well as the delivery of better medical services. Connected devices can transform the way healthcare professionals operate by allowing remote diagnosis and more efficient means of treatment. For example, patient information could be sent to hospitals via mobile and internet applications, thus saving travel time and service costs, and also substantially improving access to healthcare, especially for rural populations. Connectivity and associated devices and services could complement and improve existing medical facilities. From the citizen side, the monitoring of illnesses can also be enhanced by mobile and internet applications designed to remind patients of their treatments, and to control the distribution of medicinal stocks.

-

Energy and environment: one of the projected impacts of digitalisation is an improved ability to optimise energy utilisation and minimise environmental footprints. Connectivity and interoperability are critical elements of the information and communications technology (ICT) infrastructure that is essential to allow such optimisation and minimisation. The size of the energy efficiency market was estimated at US $221 billion in 2015, which was 14% of the global energy supply investments (IEA, 2016b), divided between buildings (53%) transport (29%) and industry (18%) (IEA, 2016a).

-

For autonomous and automated driving advanced connectivity solutions are needed with key characteristics ultra-high reliability, extremely low latency and high throughput solutions. Advanced edge solutions that will integrate AI/ML schemes over secure links will be also of paramount importance.

-

Improve public services, social cohesion and digital inclusion: ICT technologies have long been recognised as promoting and facilitating social inclusion – i.e. the participation of individuals and groups in society’s political, economic and societal processes. One way in which ICT technologies can expand inclusion is through effective public services that rely on ICT infrastructure, and through digital inclusion (i.e. the ability of people to use technology). These three aspects are deeply intertwined, and span dimensions as diverse as disaster relief, food security and the environment, as well as citizenship, community cohesion, self-expression and equality. Public authorities can enhance disaster relief efforts by promoting the spread of information online and by implementing early warning systems. The internet also enables relief efforts through crowd- sourcing: for instance, during Typhoon Haiyan in the Philippines, victims, witnesses and aid workers used the web to generate interactive catastrophe maps through free and downloadable software, helping disseminate information and reduce the vulnerability of people affected by the disaster. Communities can also be strengthened by connectivity, thereby promoting the inclusion of marginalised groups.

-

Pandemic and natural disaster management: the growing demand for remote interactions amid the coronavirus pandemic has highlighted a need for connectivity technology, potentially accelerating adoption in the mid-term of new technology such as 5G (and 6G in the 2030 time frame). Lightning-fast speeds, near- instantaneous communications and increased connection density are key to supporting massive remote interactions, which has become of increasing importance for many organisations and enterprises as anxiety rises concerning the management of health or natural disasters. Two key areas – e-health and teleconferencing – are becoming critical for enterprise operations amid pandemics or natural disasters, and an increased dependence on these areas will help strengthen the appeal of improved connectivity (for example, beyond 5G and 6G) and make connectivity a key sovereignty topic for Europe.

Beyond the above benefits to European society and economy, advanced connectivity and associated engineering and operational improvements have the potential to reduce energy and installation material footprints. For example network virtualisation will allow dynamic rearrangements of network traffic to suit changing conditions and requirements regarding e.g. energy, security and real time. In this way connectivity contributes to both the European green deal and sustainability objectives.

Improvements in connectivity technology will have an impact on all ECS application areas. For health and well-being, connectivity interoperability issues are addressed by enabling faster translation of ideas into economically viable solutions, which can be further scaled up in daily health practice. Examples of health and well-being application breakthroughs supported here are:

-

A shift in focus from acute, hospital-based care to early prevention.

-

Strengthening where and how healthcare is delivered, supporting home-based care.

-

Stronger participation of citizens in their own care processes, enhancing patient engagement.

-

Supporting the clinical workforce and healthcare consumers to embrace technology-enabled care.

-

Data communication technology for interoperability of wireless data infrastructure.

Improved, secure and interoperable connectivity will further support healthcare and well-being application breakthroughs regarding, for example:

-

Healthcare deployment, enabling digital health platforms.

-

Healthcare system paradigm transition from treatment to health prevention, enabling the shift to value-based healthcare.

-

Building a more integrated care delivery system, supporting the development of the home as the central location for the patient.

-

Enhancing access to personalised and participative treatments for chronic and lifestyle- related diseases.

-

Enabling more healthy life years for an ageing population.

In the mobility application area, the provision of improved, robust, secure and interoperable connectivity will support breakthroughs regarding: ![]()

-

Achieving the Green Deal for mobility, with the 2Zero goals of –37.5% CO2 by 2030.

-

Increasing road safety through the CCAM programme.

-

Strengthening the competitiveness of the European industrial mobility digitalisation value chain.

In the energy application domain, the provision of improved, robust, secure and interoperable connectivity will support breakthroughs regarding: ![]()

-

Significant reduction of connectivity energy demand.

-

Enabling necessary connectivity to the integration of the future heterogeneous energy grid landscape.

-

“Plug and play integration” of ECS into self-organised grids and multimodal systems.

-

Solving safety and security issues of self-organised grids and multimodal systems.

In the industry application domain, the provision of improved, robust, secure and interoperable connectivity will support closing gaps such as: ![]()

-

Preparing for the 5G era in communications technology, especially its manufacturing and engineering dimension.

-

Long-range communication technologies, optimised for machine-to-machine (M2M) communication, a large number of devices and low bit rates, are key elements in smart farming.

-

Solving IoT cybersecurity and safety problems, attestation, security-by-design, as only safe, secure and trusted platforms will survive in the industry.

-

Interoperability-by-design at the component, semantic and application levels.

-

IoT configuration and orchestration management allowing for the (semi)autonomous deployment and operation of large numbers of devices.

In the digital society application domain, the provision of improved, robust, secure and interoperable connectivity will support the overall strategy regarding: ![]()

-

Enabling workforce efficiency regardless of location.

-

Stimulating social resilience in the various member states, providing citizens with a better work/life balance and giving them freedom to also have leisure time at different locations.

-

Ubiquitous connectivity, giving people a broader employability and better protection against social or economic exclusion.

-

Enabling European governments, companies and citizens to closer cooperation, and to develop reliable societal emergency infrastructures.

In the agrifood application domain, the provision of improved, robust, secure and interoperable connectivity will support innovations addressing the EU Green Deal regarding: ![]()

-

Reducing the environmental impact related to transport, storage, packaging and food waste.

-

Reducing water pollution and greenhouse gas emission, including methane and nitrous oxide.

-

Reducing the European cumulated carbon and cropland footprint by 20% over the next 20 years, while improving climatic resilience of European agriculture and stopping biodiversity erosion.

Connectivity is currently required in almost all application fields (consumer market, automotive, health and wellbeing, smart cities, etc.), but it is worth noting that European players are stronger in terms of the IoT and secured solutions due to hardware leaders such as STMicroelectronics, NXP and Infineon, as well as solution providers such as Gemalto. On the other hand, mass market-oriented businesses such as smartphones is today dominated by the US (Qualcomm, Broadcom, etc.) or Asian players (Huawei, Murata Manufacturing, etc.), with European technology businesses being focused on system integration, digitalisation, analytics, sensors/actuators (Siemens, ABB, Schneider, Valmet, Metso, Ericsson, Nokia, Danfoss, Thales, Dassault, Philips, WV, Airbus, GKN, Skanska, BMW, Daimler, Bosch, SKF, Atlas Copco, STMicroelectronics, etc.).

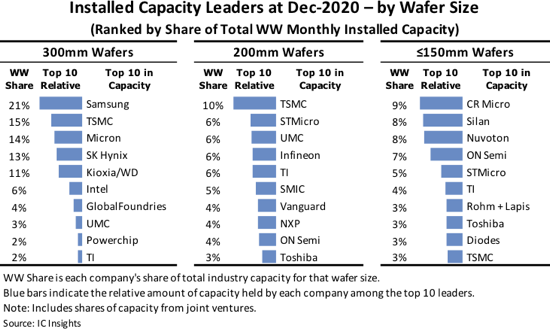

While Europe is producing only 9% of the overall electronic components (see Figure 2.2.3), its market share is 19% on the market it serves today (industry-grade embedded segments, the wireless infrastructure market being a good example with Ericsson and Nokia). This figure is in line with Europe’s GDP. Since Europe hardly addresses the consumer market, the European ecosystem requires a moderate manufacturing capacity mainly focused on mature or derivative technology. For example: automotive represents today only about 10%, but this is expected to increase in the coming years. The installed European semiconductor manufacturing capability to address Europe’s key verticals is sized accordingly, as illustrated in Figure 3: Europe has a strong presence on 200 mm facilities (with STMicroelectronics and Infineon among the top 5 leaders) which is in line with the technologies required by the European ecosystem and value chain.

The higher layer of the OSI communication stack is strongly dominated by software and network management. The European strong hold is clearly with wireless technology, (Ericsson, Nokia, ...) but also automation communication has strong European players like e.g. Siemens, ABB, Schneider, Valmet, Bosch, Endress&Hauser. For the Green deal and circularity, a major concern is the increased amount of data transferred over long distances, which need to be addressed both by technology and with solution architecture and sustainable strategies related to IoT and SoS solutions.

Consequently, to strengthen Europe’s position and enable European industry to capture new business opportunities associated with the connected world we live in, it is vital to support European technological leadership in connectivity-supporting digitisation based on IoT and SoS technologies (for example, by being at the forefront of new standard development for the current 5G initiative and the emerging SoS market). Moreover, to bring added value and differentiation compared to US and Asian competitors, European industry has to secure access to any innovative software and hardware technology that enables the efficient engineering of large and complex SoS (which will help to capture more value by targeting higher-end or more innovative applications, as highlighted by the Advancy report2).

To illustrate the competitive value for Europe of connectivity and interoperability topics, we will summarize a few of the challenges associated with the connectivity requirement in a market where European industry has been historically strong or has to secure its position for strategic reasons:

-

Automotive: the main driver here is the deployment of advanced driver-assistance systems (ADAS), which is a key opportunity for European semiconductor companies. Connectivity technology is consequently a Major Challenge since inter-sensor communication requires high bandwidth, reliability and very low latencies, and therefore innovative solutions will be necessary to prevent network overloads while meeting strict application and services requirements. A B5G and 6G networks with hierarchical architectures will be required to communicate in a reliable way with all the function domains of the car.

-

Digital production: production of goods and services already involves a multitude of data obtained from various sources. Digitalisation demands a drastic increase of data sources, ranging from sensors and simulators to models. Such data will be used for control, analytics, prediction, business logics, etc., with receivers such as actuators, decision-makers, sales and customers. Obviously, this will involve a huge number of devices with software systems that are required to be interoperable, and possible to integrate for desired combined functionality. This demands seamless and autonomous interoperability between the devices and systems involved, regardless of the chosen technology. Connectivity technology plays an important role for all application areas of the ECS-SRIA.

Five Major Challenges have been identified in the connectivity domain:

- Major Challenge 1: Strengthening the EU connectivity technology portfolio to maintain leadership, secure sovereignty and offer an independent supply chain.

- Major Challenge 2: Investigate innovative connectivity technology (new spectrum or medium) and new approaches to improving existing connectivity technology to maintain the EU’s long-term leadership.

- Major Challenge 3: Autonomous interoperability translation for communication protocol, data encoding, compression, security and information semantics

- Major Challenge 4: Architectures and reference implementations of interoperable, secure, scalable, smart and evolvable IoT and SoS connectivity.

- Major Challenge 5: Network virtualisation enabling run-time and evolvable integration, deployment and management of edge and cloud network architectures.

2.2.5.1 Major Challenge 1: Strengthening the EU connectivity technology portfolio to maintain leadership, secure sovereignty and offer an independent supply chain

Today’s connectivity solutions require an incredibly complex electronic system comprising various functions integrated into a wide range of technologies. ![]()

![]()

Note that advanced digital functions such as the application processor and the baseband modem are mastered by a limited number of US and Asian players (Hisilicon, Mediatek, Qualcomm and Samsung), and achieved in advanced complementary metal–oxide–semiconductor (CMOS) technology available at only two Asian businesses (Taiwan Semiconductor Manufacturing Company, TSMC, and Samsung). On this last point, it is worth noting that through the America CHIPS Act, Intel and TSMC will build new advanced logic (3 nm) 300 mm Fabs in Arizona while the European Chips Act should support advanced node fabrication facilities by TSMC in Dresden and by Intel in Magdeburg. The European Chips Act should also support ST and GF plans to build a new 300 mm facility in France to allow for 10 nm and beyond FDSOI technology manufacturing, all this in order to limit the reliance on Asian foundries’ manufacturing capabilities.

From their side, European players (Infineon, NXP, ST, etc.) are strong on the analogue and RF front end module markets, mainly due to the availability of differentiated technologies developed and manufactured in Europe. Differentiated technologies are a key strength of the European ECS industry, especially when considering the connectivity market.

Consequently, to maintain Europe’s leadership and competitiveness it is vital to ensure that European differentiated semiconductor technologies remain as advanced as possible. This is key to ensure that Europe secures the market share in the connectivity market, and also strengthens its technology leadership by playing a major role in the development and standardisation of future connectivity technologies. This point is crucial to secure Europe’s sovereignty on the connectivity topic.

Moreover, over the last year the rising economic tension between the US and China has underlined the value of Europe's ECS supply chain. Once again, this is especially true for differentiated technologies. For example, advanced BiCMOS technologies are currently mastered by a limited number of US (GlobalFoundries and TowerJazz) and European (Infineon, ST and NXP) players. With Chinese companies being forced to move away from US providers, this creates a significant opportunity for Europe as the only viable alternative. Consequently, strengthening Europe’s connectivity technology portfolio and associated manufacturing capacity to offer an independent and reliable supply chain is now a key challenge for all European ECS actors.

In addition to being able to provide the differentiated semiconductor technologies supporting the development of innovative connectivity solutions, it is important to note that some European players are proposing connectivity chipset solutions (for example, Sequans Communications and Nordic on the narrowband (NB) IoT topic) or full connectivity solutions. Supporting the growth of these existing actors and helping emerging industry leaders is also a key challenge for Europe to capture a bigger proportion of the value chain, as well as to ensure its sovereignty on the connectivity topic in the long run.

To address identified connectivity technology challenges, we propose the vision described below, which can be summarised by the following three key points (with associated expected outcomes).

Strengthening Europe’s differentiated technologies portfolio

As discussed above, Europe’s differentiated semiconductor technologies are key assets that should be both preserved and improved upon to secure European leadership in connectivity. Consequently, dedicated research should be encouraged, such as the technologies below (which are also promoted in the Chapter 1.1 on Process Technology, Equipment, Materials and Manufacturing): ![]()

-

Advanced BiCMOS: targeting RF and sub-THz (i.e., 100-300GHz) and THz front-end modules.

-

RF SOI: targeting <7 GHz and mmW front-end modules.

-

GaN: targeting the high-power infrastructure and high efficiency/wide bandwidth 6G handset markets (5.925 GHz – 7.125 GHz and 10 GHz – 13.25 GHz bands).

-

FD SOI: targeting power-efficient connectivity solutions (for example NB IOT and NTN).

-

GaAs: targeting mmW space and defense applications ( W & K bands).

-

InP & InP on Si: targeting high-speed optical link (>800 Gb/s), mmW applications (6G sub-THz communication >100 GHz) and ultra-low noise Front End Module in K band.

-

RF filters: supporting the development on innovative European based technology (for example POI based TF SAW technologies).

-

Advanced packaging: enabling prototyping and medium volume production capability in Europe to enable Heterogeneous integration of differentiated technology manufacture in Europe to move higher in the value chain and capture more value.

The main challenge will be in improving achievable performances. To illustrate this, we have extracted the medium-term (2025) and long-term (2030) solid state technology roadmap proposed by H2020 CSA project NEREID to serve as a connectivity roadmap (see Figure 2.2.4). We can see that whatever the type of application (device-to-device, D2D, indoor, outdoor), the requirements in analogue RF will mainly consist of achieving Fmax and FT ~500 GHz in 2025 and 1 THz in 2030, while NFmin will be well below 1 dB in the medium term, to reach 0.5dB in the long term. The only parameter that differentiates the types of applications is the output power, which outdoors should reach between 36 and 40 dBm per PA by the end of the decade. The biggest challenge for silicon or hybrid-on-silicon substrate technologies is expected to be the frequency challenge. Technologies such as GaN/Si and RF SOI will deliver power but for applications operating at less than 100 GHz.

Note that the vision presented in Figure 2.2.4 also applies to packaging and printed circuit board (PCB) technologies. It is also worth noting that while Europe is playing a key role in innovative differentiated semiconductor technologies, there is very little R&D activity or few players in Europe on the packaging and PCB side. This point is clearly a weakness that should be addressed to strengthen Europe’s connectivity technology portfolio.

Securing Europe’s differentiated hardware technology manufacturing

Beyond the development and enablement in Europe of innovative semiconductor technologies targeting the connectivity market, it will be key to safeguard and promote European manufacturing capability to both secure Europe economical interest (in terms of market share) and also address the sovereignty topic (since trade war issues can jeopardise the viability of Europe’s industrial actors). To do so, in coordination with chapter 1.1 on Process Technology, Equipment, Materials and Manufacturing, the following topics should be supported: ![]()

-

The enablement of pilot lines: the objective here is to support the deployment of additional manufacturing capabilities for technology already available in Europe (supporting the transition to 300 mm Fab), or to address new technologies (such as packaging or advanced PCB) to increase the technology portfolio available in Europe.

-

The rise of new semiconductor equipment champions: to secure manufacturing capabilities in the long term, it will also be necessary to ensure that the required equipment is provided by European players. This is crucial to prevent any vulnerability in the European supply chain to possible international political or economic issues.

-

Nurture a pan-European design ecosystem to tackle the new challenges on transistors in more than Moore, circuits architectures with increased security and trustworthiness and new AI/ML chips raised by the digitalisation era.

Strengthening Europe’s connectivity technology portfolio (hardware, internet protocols and software)

Leveraging previously discussed differentiated semiconductor technology portfolio, innovative connectivity solutions (hardware, internet protocol (IP) or software) should be encouraged to enable Europe to take full advantage of its technology and manufacturing assets, and to capture market share at the component level. This action is crucial to secure Europe's position beyond 5G and preliminary 6G investigation and standardisation activities. It also enables the development and manufacturing in Europe of highly integrated connectivity module/systems.

Since most of the value of a complex connectivity system will be captured at the module level, it is highly desirable to enable European players to rise the value chain (in coordination with the chapter Components, Modules and Systems Integration). ![]()

In targeting systems and applications, it is important to consider the interconnection between subsystems, and focus should be on individual component technology development according to needs identified at the system or application level. To support this system vision, the promotion of innovative technology enabling heterogeneous integration is key.

Heterogeneous integration refers to the integration of separately manufactured components into a higher- level assembly that cumulatively provides enhanced functionality and improved operating characteristics. In this definition, components should be taken to mean any unit – whether individual die, device, component, and assembly or subsystem – that is integrated into a single system. The operating characteristics should also be taken in their broadest meaning, including characteristics such as system-level cost of ownership.

This is especially true for the hardware side in the context of the end of Moore’s law. It is the interconnection of the transistors and other components in the integrated circuit (IC), package or PCB and at the system and global network level where future limitations in terms of performance, power, latency and cost reside. Overcoming these limitations will require the heterogeneous integration of different materials (silicon, III-V, SiC, etc.), devices (logic, memory, sensors, RF, analogue, etc) and technologies (electronics, photonics, MEMS and sensors).

To support the vision presented in the previous paragraph, we propose to focus effort on the following key focus areas:

-

Innovative materials (GaN, InP, etc.) and large diameter wafers technology (POI, InP on Si, GaN on Si, InP etc.) supporting the development of innovative connectivity technology solution.

-

Innovative differentiated semiconductor technology development targeting connectivity application.

-

Innovative packaging and PCB technology targeting connectivity application.

-

Pilot line enablement to support the strengthening of European manufacturing capability.

-

Innovative semiconductor equipment enablement.

-

Innovative connectivity solution engineering through virtualisation of the different connectivity layers.

-

Enable a European ecosystem that can support heterogeneous integration (multi-die system in a package, advanced assembly capability, advanced substrate manufacturing, etc.) to help European players capture higher value in the connectivity market.

-

Ultra‐low power transceivers will be needed, and low eco‐footprint.

-

Power efficient and cost efficient transceivers including Data conversion (ADC-DAC), up & down frequency conversion (LO & mixers), and RF emission and Reception (PA-LNA).

-

Antennas and packages at mm‐wave and THz, on‐chip antennas.

-

Advanced System on Chip design for CMOS and new technologies like e.g. GaN, InP, InP on Si, GaN on Si.

-

Meta-materials for antennas, meta‐materials for intelligent reflective surfaces and meta‐surfaces.

2.2.5.2 Major Challenge 2: Investigate innovative connectivity technology (new spectrum or medium) and new approaches to improving existing connectivity technology to maintain the EU’s long-term leadership

Targeting connectivity solutions beyond 5G, R&D activity is today mainly focused on the three key challenges listed below. ![]()

![]()

Evaluating the advantage to use new spectrum (especially 7 GHz – 20 GHz band and mmW frequencies >100 GHz)

With the ongoing deployment of 5G in the <6 GHz and 28 GHz bands, the current R&D focus is now on the spectrum considered for 6G development targeting the 2030 time horizon. Three main frequency bands are today discussed in the telecommunication industry:

Low band (5.925 GHz – 7.125 GHz):

This band is attracting a lot of attention for 6G (especially in China), we can note that some competition exist with future Wi-Fi development. While China allocated the full band for IMT services, the US did the opposite and the FCC allocated the band for Wi-Fi. Europe is considering an intermediate stance and will likely allocate the 5.925 – 6.425 GHz range to Wi-Fi and the 6.425 GHz – 7.125 GHz range for IMT. Development of wireless system in this band will likely be incremental to previous one <6 GHz, however we can mention that PA efficiency (GaN opportunity on the handset market?) and filtering technology (due to coexistence issues with Wi-Fi) seem the main challenges today.

Mid band (10 GHz – 13.25 GHz):

While no regulation has been enacted yet, the 7 GHz – 20 GHz spectrum is attracting a lot of attention (compared with 3.5 GHz, propagation attenuation will be increased in an acceptable range while path loss will be further reduced by more advanced radio technologies. ). Eliane Semaan, director of spectrum and technology regulation for infrastructure vendor Ericsson, wrote in 20224: "Spectrum from within the 7-20 GHz range is essential to realize the capacity-demanding use cases in future 6G networks". Nokia is pushing the same view, Harri Holma and Harish Viswanathan also wrote in 20225: "Ten years from now we expect new spectrum bands between 7 GHz and 20 GHz to open up for 6G use, which will provide the necessary bandwidth to create these new high-capacity carriers," We can note that Huawei is also pursuing the same strategy but is more specific on the 10 GHz – 13.25 GHz spectrum6. This band seems one of the most promising since Jessica Rosenworcel, chairwoman of the FCC, recently said she's eyeing the 12.7GHz to 13.25GHz spectrum band as a possible location for the agency's next big spectrum push. From hardware technology point of view, working over 10 GHz will bring several challenges. From PA side, we can wonder if GaAs HBT technology will remain relevant. From filter side, It is not clear if existing filter technologies will provide acceptable performances. More generally, it creates an opportunity for SiGe technology (and consequently for Europe) since this technology is today widely used in the X and Ku bands for satellite communication.

NTN Mid band (Ku band: 12 GHz – 18 GHz & Ka and FWA band: 28 GHz – 40 GHz):

In addition to new spectrum requirements previously mentioned, 6G envision to seamlessly integrate existing satellite communication in cellular connectivity networks. This trend can be seen under the topic Non Terrestrial Networks currently discussed inside 3GPP.

Targeted frequency spectrum is not new (traditional Ku and Ka bands). The main objective is here to leverage under redeployment Low Earth Orbit satellite constellation to complement the cellular network coverage while offering performances (latency & data rate) in line with real-time application.

Two main challenges will have to be addressed: seamless integration and handover of satellite connectivity along with cellular one (network type should be transparent for the user) and the development of cost-effective chipset solutions to enable user terminals in line with mass market constraints (which creates key opportunities for Si-based technology such as SiGe BiCMOS).

High band (>100 GHz):

While the R&D evaluation has been focused on frequencies below 20 GHz to date, there is now some interest in assessing achievable performances with a higher frequency. For regulatory reasons, the 275 GHz – 325 GHz range holds promise as it enables the widest available bandwidth. As an illustration, to play a key role in preliminary 6G investigations, the US has facilitated their research on the 95 GHz – 3 THz spectrum over the coming decade. After a unanimous vote, the Federal Communications Commission (FCC) has opened up the “terahertz wave” spectrum for experimental purposes, creating legal ways for companies to test and sell post-5G wireless equipment. However, we can note that the telecommunication industry is cautious on the use of this spectrum. Magnus Frodigh, Ericsson's chief researcher, for example wrote7: "We have thus identified new potential spectrum ranges for 6G, notably in the centimetric range from 7-15 GHz, which we believe will be an essential range, and in the sub-THz range from 92-300 GHz, which will have a complementary role serving niche scenarios". He continued: "Our learnings from 5G are that the mmWave range is a powerful spectrum range which allows operators to provide value to industry and enterprise through high data rates. However, due to limited coverage, it serves as a complement to other ranges that can be used in wider areas but with limited data rates (i.e. mid bands)." Frodigh concluded: "We believe that in order to benefit society, the majority of 6G use cases should be enabled for wide-area coverage, both indoors and outdoors, and not limited to confined areas. This means that – whilst we ought to explore the sub-THz region for entirely novel 6G capabilities – the main value will be in the centimetric 7-15 GHz". At such high frequency, new hardware technology may be required and InP is today a hot topic to enable low noise receivers and power efficient Power Amplifiers > 100 GHz.

Evaluating the opportunity to use new medium of propagation

Over the last few years, impressive results have been reported concerning high-speed millimetre wave silicon transceivers coupled to plastic waveguides. The state of art on the data rate is now at 36 Gb/s, with a short distance of 1 m in SiGe 55 nm BiCMOS with 6pJ/b.meter working at 130 GHz. The maximum distance ever reported is 15 m, with 1.5 Gb/s data rate using 40nm CMOS at 120 GHz. In the 10 m distance – which, for instance, is the requirement for data centre applications – the state of the art is given by a data rate of 7.6 Gb/s at 120 GHz for 8m in 40nm CMOS, and a data rate of 6 Gb/s at 60 GHz for 12m in 65 nm CMOS. Although a 10 Gbps data rate, seems feasible, questions remain over whether there is the required energy per bit to deliver this performance. Interesting technologies here is intelligent reflective surfaces and meta surfaces. ![]()

Exploring the benefits that AI could bring to connectivity technologies

While 5G is being deployed around the world, efforts by both industry and academia have started to investigate beyond 5G to conceptualise 6G. 6G is expected to undergo an unprecedented transformation that will make it substantially different from the previous generations of wireless cellular systems. 6G may go beyond mobile internet and will be required to support ubiquitous AI services from the core to the end devices of the network. Meanwhile, AI will play a critical role in designing and optimising 6G architectures, protocols and operations.

For example, two key 5G technologies are software-defined networking (SDN) and network functions virtualisation (NFV), which have moved modern communications networks towards software-based virtual networks. As 6G networks are expected to be more complex and heterogeneous, advanced softwarisation solutions are needed for beyond 5G networks and 6G networks. Selecting the most suitable computational and network resources and the appropriate dynamic placement of network functions, taking network and application performance as well as power consumption and security requirements into account, will be an important topic. By enabling fast learning and adaptation, AI-based methods will render networks a lot more versatile in 6G systems. The design of the 6G architecture should follow an “AI-native” approach that will allow the network to be smart, agile, and able to learn and adapt itself according to changing network dynamics.

To address identified connectivity technology challenges, we propose the vision described below, which can be summarised in the following three points (with associated expected outcomes).

Assess achievable connectivity performances using new spectrums

To maintain European leadership on connectivity technology and ensure sovereignty, the development of new electronics systems targeting connectivity applications in non-already standardised (or in the process of being standardised) spectrums should be supported. A special focus should be dedicated to the frequency bands listed below.

-

Sub-THz connectivity application in the 200 GHz – 300 GHz band: With THz communication being a hot topic in the international community, European activity in the spectrum > 300 GHz should be encouraged. These investigations should help Europe play a role in the development of the new technology and assess its relevance to future 6G standards.

-

Unlicensed connectivity in the 6 GHz – 7 GHz band: As Wi-Fi 6 is currently being deployed in the US in the 5 GHz – 6.2 GHz band (on April 23 2020, the FCC approved the opening of 1200 MHz of spectrum to IEEE 802.11ax), this spectrum allocation is also under discussion in Europe. It is vital for Europe to support investigations on this frequency band to ensure that the next generation of Wi-Fi technology is accessible to European citizen and businesses (without any limitation compared to other countries).

-

Investigation of the <10 GHz spectrum for 6G: While 5G was initially thought to be mainly linked to the mmW spectrum (for example, at 28 GHz), most of the current deployment effort is happening in the new < 6 GHz frequency bands. To complement the investigation of the above-mentioned THz communication, the evaluation and development of innovative connectivity technology <10 GHz should be encouraged. This may secure European leadership in future 6G proposals and standardisation activities.

Investigate new propagation medium to enable power-efficient and innovative connectivity technologies

New applications create the need for new connectivity technology. For example, autonomous driving requires very high-speed communication (currently 10 Gb/s and 40 Gb/s in the future) to connect all the required sensors to the central processing unit (CPU). While Ethernet is today perceived as the technology of choice, its deployment in cars is challenging since the electromagnetic interference (EMI) requirements of the automotive industry impose the use of shielded twisted pairs, which add cost and weight constraints. To address this need, intense R&D activity has been pursued over the last few years to assess the relevance of mmW connectivity using plastic waveguides (as described in the previous section). Consequently, the development of innovative connectivity solutions using new mediums of propagation should be encouraged to enable innovative connectivity technology and ensure European leadership and sovereignty.

Integrate AI features to make connectivity technology faster, smarter and more power-efficient

The use of new spectrums or propagation mediums is not the only way to boost innovative connectivity technology. As mentioned, 5G has underlined the role of software to promote virtualisation and reconfigurability, but those concepts may not be sufficient to address the challenges related to the more complex connectivity technology that may be developed (for example, 6G). ![]()

![]()

To address this challenge, Artificial Intelligence is now perceived as a strong enabler. Consequently, in coordination with the “Edge Computing and Embedded Artificial Intelligence” chapter, the topics below should be supported. ![]()

-

Investigate AI features at the edge: to improve the power efficiency of mobile devices by reducing the amount of data to be transmitted via the wireless network, the concept of AI at the edge (or edge AI) has been proposed. The idea is to locally process the data provided by the sensor using mobile device computing capability. Moreover, processing data locally avoids the problem of streaming and storing a lot of data to the cloud, which could create some vulnerabilities from a data privacy perspective.

-

Use AI to make the connectivity network more agile and efficient: the idea here is to move to an AI-empowered connectivity network to go beyond the concept of virtualisation and achieve new improvements in terms of efficiency and adaptability. For example, AI could play a critical role in designing and optimising 6G architectures, protocols and operations (e.g. resource management, power consumption, improved network performance etc.).

To support the vision presented in the previous paragraph, we propose that efforts should be focused on the following key focus areas:

-

Innovative connectivity system design using new spectrums (especially mmW).

-

Investigation and standardisation activity targeting 6G cellular application in the frequency band < 10 GHz.

-

Development of innovative connectivity technology using unlicensed frequencies in the 6 GHz – 20 GHz band.

-

Development of innovative connectivity systems using new propagation mediums.

-

Development of connectivity system leveraging the concept of edge AI.

-

Evaluation of the AI concept to handle the complexity of future connectivity networks (for example, 6G), and to improve efficiency and adaptability.

2.2.5.3 Major Challenge 3: Autonomous interoperability translation for communication protocol, data encoding, compression, security and information semantics

Europe has a very clear technology lead in automation and digitalisation technology for industrial use. The next generation of automation technology is now being pushed by Industry 4.0 initiatives backed by the EC and most EU countries. In the automotive sector, the autonomous and green car vision is the driver. Here, Europe again has a strong competitive position. In healthcare, the ageing population is the driver. Europe’s position in this area is respectable but fragmented. Robust, dependable, secure and interoperable connectivity from application to application and prepared for interaction in System of Systems solution are fundamental to market success in these and other areas. ![]()

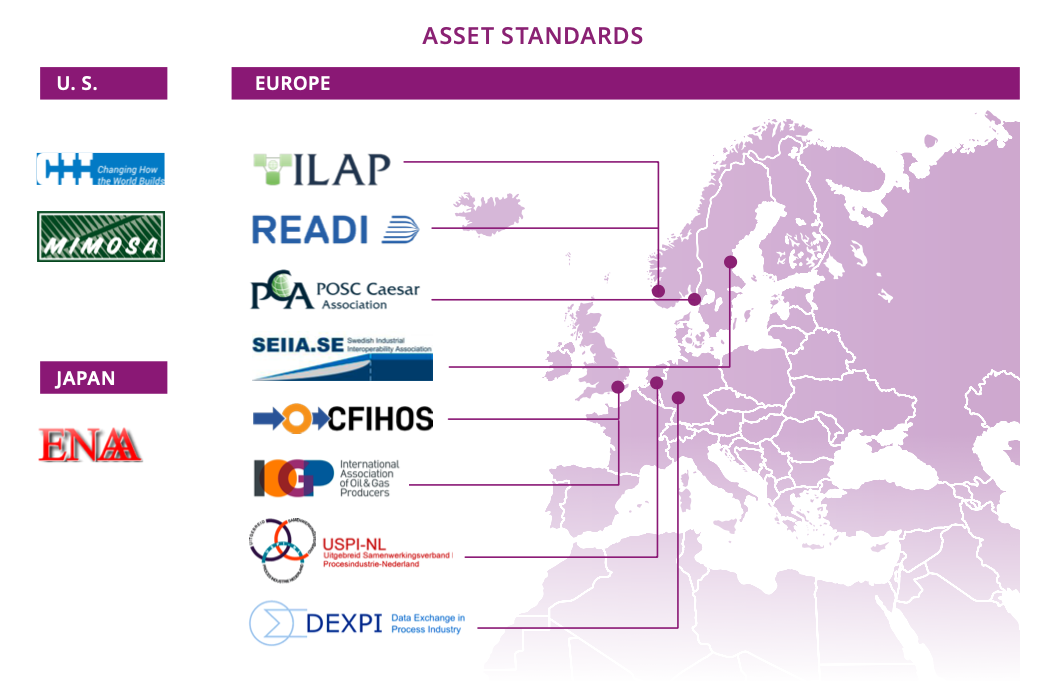

Interoperability is a growing concern among numerous industrial players. An example here is the formation of industrial alliances and associated interoperability project efforts. One of the directions chosen targets is to gather behind a few large standards. An example of this is showcased in Figure 2.2.6.

To maintain and strengthen the European lead, advances in autonomous interoperability and associated efficient engineering capability are necessary. The game changers are:

-

Autonomous interoperability for SoS integration for efficient machine supported engineering at design-time and run-time.

-

Open interoperability frameworks and engineering platforms.

-

Novel, flexible and manageable security solutions.

-

Standardisation of the above technologies.

To fully leverage heterogeneous integration at the hardware level, software interoperability is a parallel challenge to provide application to application connectivity that allows for autonomous SoS connectivity, from edge to cloud, enabling usage of available data for all areas of application. To do so, dedicated software tools, reference architecture and standardisation are key to supporting autonomous interoperability, thus enabling the provision of a widely interoperable, secure, scalable, smart and evolvable SoS connectivity.

This challenge involves the interoperability of service or agent protocols, including encoding, security and semantics. Here, payload semantics interoperability is a primary focus, leading to architectures, technologies and engineering tools that support application to application integration of SoS for all areas of applications at design- time, in run-time and over life cycle. This will include e.g. translation between different standards used in domains where SoS interaction is necessary to reach business and societal objectives.

The objective here is a technology that enables nearly lossless interoperability across protocols, encodings and semantics, while providing technology and engineering support foundations for the low-cost integration of very large, complex and evolvable SoS.

Expected achievements are:

-

Open source implementation of reference architectures supporting interoperability, security scalability, smartness and evolvability across multiple technology platforms, including 5G & 6G.

-

Open source engineering and implementation frameworks for the de-facto standard SoS connectivity architecture.

-

Architecture reference implementations with performance that meets critical performance requirements in focused application areas.

The high-priority technical and scientific challenges in both design-time and run-time are:

-

Semantics interoperability from application to application.

-

Autonomous translation of protocols, encodings, security and semantics.

-

Evolvable SoS connectivity architectures and technologies over time and technology generations.

2.2.5.4 Major Challenge 4: Architectures and reference implementations of interoperable, secure, scalable, smart and evolvable IoT and SoS connectivity

It is clear that the US is the leader when it comes to wired connectivity while Europe is the leader in cellular connectivity. The big potential game changer here is 5G and upcoming 6G. To advance the European position, the establishment of connectivity architecture, reference implementation and associated engineering frameworks supporting 5G/6G and other wireless technologies is required. The primary application markets should connect to European strongholds such as automation, digitalisation and automotive. The game changers are:

-

Establishment of connectivity architecture standards with associated reference implementation and related engineering frameworks.

-

SoS application to application connectivity being interoperable, secure, scalable, smart and evolvable over technology generations.

The enabling of SoS connectivity is fundamental for capturing the emerging SoS market and its very high growth rate. Efficient engineering and the deployment of interoperable, secure, scalable, smart and evolvable SoS connectivity will be key to this. This will help Europe lead in the establishment of connectivity architecture, reference implementation and associated engineering frameworks. ![]()

In certain domains such as automotive and industrial automation, Europe is the major player. Market studies8 indicate very large to extreme growth in the SoS market over the next five years.

This will provide a very strong market pull for all technologies and products upstream. Here, connectivity interoperability is a very important component, enabling tailored SoS solutions and efficient engineering. The vision is to provide interoperable connectivity architecture, reference implementation and associated engineering support and frameworks spanning technologies from legacy to 5G and 6G and other wireless and wired technologies.

Expected achievements

-

Open source implementation of reference architectures supporting interoperability, security scalability, smartness and evolvability across multiple technology platforms, like e.g. 5G/6G, wired and optical connectivity.

-

Open source engineering and implementation frameworks for the de-facto standard SoS connectivity architecture.

-

Architecture reference implementations which meet critical performance requirements in focused application areas.

The high-priority technical and scientific challenges are:

-

SoS connectivity architecture as a de-facto standard.

-

Reference implementation of de-facto SoS connectivity architectures.

-

Engineering frameworks for de-facto standard SoS connectivity architecture.

2.2.5.5 Major Challenge 5: Network virtualisation enabling run-time engineering, deployment and management of edge and cloud network architectures

Virtualisation of networks is a main trend for cellular networks. This has to be expanded to other wireless and wired connectivity technology. The game changers are: ![]()

![]()

-

Technologies for network virtualisation across multiple hardware and software layers using heterogeneous devices.

-

Engineering and integration tools and management methodologies for efficiently engineering, integration and management of virtualized IoT and SoS networks and service components.

-

Intelligent, configurable generic hardware platforms.

The enabling of virtualised networks is fundamental for capturing the emerging SoS market and its very high growth rate. Efficient engineering, deployment and management of connectivity is a key enabler for interoperable, secure, scalable, smart and evolvable SoS. This will help Europe lead in the establishment of connectivity architecture, reference implementation and associated engineering frameworks.

European leadership in certain domains, mentioned above, will provide a very strong market pull for all technologies and products upstream. Here, virtualised connectivity is a very important component, enabling dynamic updates and rearrangements of SoS solutions. The vision is to provide virtualised connectivity across physical and mac layers spanning technologies from legacy to 5G and upcoming 6G.

Expected achievements:

-

Open source implementation of reference architectures supporting virtualised connectivity across multiple technology platforms, including 5G, B5G, 6G, wired and optical.

-

Open source engineering and management frameworks for virtualised connectivity across multiple technology platforms, including 5G, B5G, 6G, wired and optical.

-

Reference implementations with performance that meets critical performance requirements in focused application areas taking into consideration energy efficiency.

The high-priority technical and scientific challenges are:

-

Virtual connectivity architecture supporting multiple technology platforms.

-

Reference implementation of virtual connectivity architecture enabling very efficient application-level usage.

-

Engineering, integration and management frameworks with tools for virtual connectivity architectures.

The timeline for addressing the Major Challenges in this section is provided in the following table.

| MAJOR CHALLENGE | TOPIC | SHORT TERM (2024–2028) | MEDIUM TERM (2029–2033) | LONG TERM (2034 and beyond) |

|---|---|---|---|---|

|

Major Challenge 1: Strengthening the EU connectivity technology portfolio to maintain leadership, secure sovereignty and offer an independent supply chain |

Topic 1.1: innovative differentiated semiconductor technology development targeting connectivity application |

TRL 4–6 Enable next generation RF SOI and BiCMOS technology as well as innovative GaN on Si technology |

TRL 7–9 Industrial transfer of previous technologies from pilot line to Fab |

|

| Topic 1.2: innovative packaging and PCB technology targeting connectivity application |

TRL 3–4 Development of innovative European packaging (such AMP) and PCB technologies |

TRL 5–6 Pilot line enablement and support of small series |

TRL 7–9 | |

| Topic 1.3: pilot line enablement to support European manufacturing capability strengthening |

TRL 4–6 Support the transition from 200 mm to 300 mm for existing technologies |

TRL 7–9 Add manufacturing capability beyond existing technologies |

||

| Topic 1.4: innovative semiconductor equipment enablement | TRL 3–4 | TRL 5–6 | TRL 7–9 | |

| Topic 1.5: innovative connectivity solution development targeting hardware, IP and software items | TRL 3–4 | TRL 5–6 | TRL 7–9 | |

| Topic 1.6: enable a European ecosystem that can support heterogeneous integration (multi-die system in a package, advanced assembly capability, advanced substrate manufacturing, etc) to help European players capture higher value in the connectivity market |

TRL 4–6 Ease the access to existing pilot line and enable associated IP ecosystem |

TRL 7–9 From pilot line to industrial manufacturing |

||

|

Major Challenge 2: Investigate innovative connectivity technology (new spectrum or medium) and new approaches to improving existing connectivity technology to maintain the EU’s long-term leadership |

Topic 2.1: innovative connectivity system design using new spectrums (especially mmW) |

TRL 3–4 Assess the specification of wireless systems in the 200 GHz – 300 GHz band |

TRL 5–6 Achieve preliminary transceiver demonstrator using European technologies |

TRL 7–9 Transfer to the industry to enable European products |

| Topic 2.2: investigation and standardisation activity targeting 6G cellular application in frequency band < 10 GHz |

TRL 3–4 Contribute to 6G mid band spectrum standardisation |

TRL 5–6 Leverage European differentiated technologies to address 6G mid band spectrum challenges |

TRL 7–9 Enable first 6G connectivity chipset solution |

|

| Topic 2.3: development of innovative connectivity technology using unlicensed frequency in the 6 GHz – 7 GHz band |

TRL 4–6 Contribute to Wi-Fi6E and 7 standardisation |

TRL 7–9 Enablement of European Wi-Fi 6E and 7 chipset solution leveraging European derivative technology |

||

| Topic 2.4: development of innovative connectivity systems using new propagation mediums | TRL 3–4 | TRL 5–6 | TRL 7–9 | |

| Topic 2.5: development of connectivity systems leveraging the concept of edge AI | TRL 4–6 | TRL 7–9 | ||

| Topic 2.6: evaluation of the AI concept to be able to handle the complexity of future connectivity networks (for example, 6G), and to improve efficiency and adaptability | TRL 4–6 | TRL 7–9 | ||

|

Major Challenge 3: Autonomous interoperability translation for communication protocol, data encoding, compression, security and information semantics |

Topic 3.1: semantics interoperability | AI-supported translation of payload semantics based on a limited set of ontologies and semantics standards | General translation of payload semantics enabling application information usage | General translation of payload semantics enabling application information usage |

| Topic 3.2: autonomous translation of protocols, encodings, security and semantics | Autonomous and dynamic translation between SOA-based services protocol, data encoding, data compression and data encryption | Dynamic translation between major data model relevant for the ECSEL field of application. | Autonomous and dynamic translation between a large set of data models relevant for the ECSEL field of application | |

| Topic 3.3: evolvable SoS connectivity architectures and technologies over time and technology generations | TRL4–6 | TRL 5–7 | TRL6–8 | |

|

Major Challenge 4: architectures and reference implementations of interoperable, secure, scalable, smart and evolvable IoT and SoS connectivity |

Topic 4.1: SoS connectivity architecture as a de facto standard | SoS connectivity architecture based on SOA established as a major industrial choice in the application domains of the SRIA | SoS connectivity architecture based on SOA established as the major industrial choice in the application domains of the SRIA | |

| Topic 4.2: reference implementation of de facto SoS connectivity architectures | Reference implementation of the SoS connectivity architecture becoming a natural part of the global SoS architecture (chapter SoS) reference implementation | Reference implementation of the SoS connectivity architecture becoming a natural part of the global SoS architecture (chapter SoS) reference implementation at TRL 8–9. | ||

| Topic 4.3: engineering frameworks for de facto standard SoS connectivity architecture | Reference implementation of an engineering framework with associated tools for SoS connectivity | Reference implementation of an engineering framework with associated tools for SoS connectivity at TRL 8 | ||

|

Major Challenge 5: network virtualisation enabling run-time engineering, integration, deployment and management of edge and cloud network architectures |

Topic 5.1: Virtual connectivity architecture supporting multiple technology platforms, including 5G, B5G and 6G AI |

TRL-3-5 a fully distributed edge environment, including hardware accelerators

|

TRL 5-7 | TRL 6-8 |

| Topic 5.2: Reference implementation of virtual connectivity architecture |

TRL 3-5 Edge modules, integration of multiple technologies for JCAS, Flexible hardware platforms supporting virtualisation and programmability in a fully distributed edge environment |

TRL 5-7 Pilot scale demonstrations fully distributed edge environment, including hardware accelerators to significant lower cost levels compared to current industrial SOTA |

TRL6-8 | |

|

Topic 5.3 Engineering, integration and management frameworks |

Advanced baseband capabilities in open virtualisation platforms from hardware(e.g. RISC-V) to open software integration and virtualisation platforms | TRL 5-7 | TRL6-8 |

In order to speed up the pace at which research results may be brought to the market, clear links can be underlined between the proposed SRIA on connectivity and “innovation accelerators” being currently set up in the frame of the European Chips Act. We refer here specifically to the Design Platform and the Pilot Lines included in the Chips for Europe Initiative, which have the objective of supporting technological capacity building and innovation in the Union by bridging the gap between the Union’s advanced research and innovation capabilities and their industrial exploitation.

Being more specific to the context of this SRIA connectivity chapter, the following synergies can be mentioned (according to ongoing discussions about the Chips for Europe initiative at the time of the writing of this chapter):

-

Heterogeneous Integration and Advanced Packaging Pilot Line: this initiative should support the R&I efforts in the following key focus areas of Major Challenge 1 (see 2.2.5.1.3 key focus areas).

-

Enable a European ecosystem that can support heterogeneous integration (multi-die system-in-a-package, advanced assembly capability, advanced substrate manufacturing, etc.) to help European players capture higher value in the connectivity market.

-

Enable the development of innovative antenna-in-package solutions at mm-wave and THz frequencies.

-

Enable a sovereign European packaging ecosystem to secure the supply chain of European semiconductor players (especially in key areas such as space were required manufacturing scale limits the possibility to have access to Asian OSAT)

-

-

FDSOI Pilot Line: this initiative should support the R&I efforts in the following key focus areas of Major Challenge 1 and 2 (see 2.2.5.1.3 key focus areas).

-

Enable the development of power efficient connectivity solution leveraging European based semiconductor technology.

-

Enable the development of innovative connectivity solution at mmW and THz frequencies.

-